What UAE Businesses Need to Know:

As a person in the business world, you have probably heard of ECL and IFRS 9. Let us break that down:

What is ECL?

Expected Credit Loss (ECL) under IFRS 9 is a feature of modern financial reporting. It helps businesses prepare for risks by predicting potential credit losses. Following ECL requirements and implementing ECL is a way to calculate the risk of customers not paying back what they owe. The goal is to predict losses early, not wait for them to happen.

What is IFRS 9?

IFRS 9 is a global accounting standard focusing on financial instruments such as loans, trade receivables, and investments. It replaced IAS 39 and introduced the ECL model, which has gained popularity for its progressive design. Businesses can now predict potential losses before they happen instead of waiting for defaults with ECL.

Why Does IFRS 9 Matter to UAE Businesses?

- Ensures financial statements reflect REAL risks.

- Align your business with global accounting practices.

- Builds trust with investors and regulators.

How is ECL calculated?

Expected Credit Loss (ECL) is a way to estimate potential losses on loans and receivables. You can calculate ECL using the following:

ECL=PD×LGD×EAD\text{ECL} = \text{PD} \times \text{LGD} \times \text{EAD}

- PD (Probability of Default): The likelihood that a customer won’t pay.

- LGD (Loss Given Default): The amount lost if they default.

- EAD (Exposure at Default): How much they owe.

Example: Your business has a customer owing AED 200,000 with:

- PD = 2%

- LGD = 40%

ECL = 200,000×0.02×0.4=AED1,600 200,000 \times 0.02 \times 0.4 = AED 1,600

You should account for AED 1,600 as a potential loss.

Simplified vs. General Approach

You have the Simplified and General Approaches for calculating Expected Credit Loss (ECL)

Simplified

The Simplified Approach suits more straightforward assets quicker, while the General Approach is more detailed and adapts to complex or long-term credits.

The simplified Approach is used for trade receivables or contract assets and directly calculates lifetime ECL without categorising stages.

General Approach

The general Approach is used for loans or long-term credit and categorises assets into stages based on credit risk.

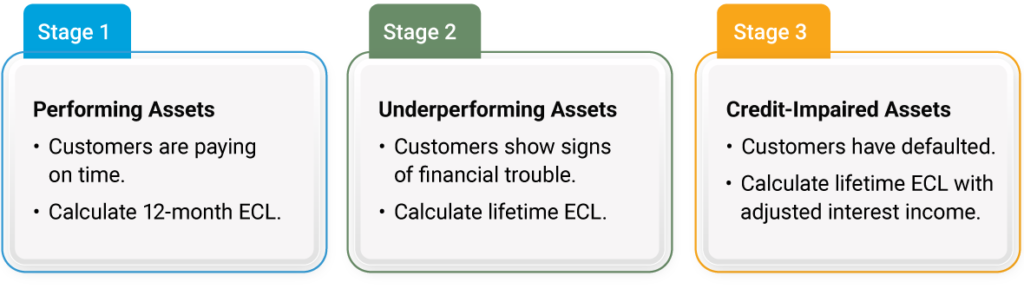

Stages of ECL Calculation

The stages for ECL under IFRS 9 warn of the increase in credit risk of financial assets. These stages allow you to make the required provisions. Thus, predicting the risk stage helps recognise losses more accurately.

IFRS 9 divides financial assets into three categories:

IFRS 9, ECL AND THE UAE – Long story cut short:

For UAE businesses, the Central Bank of the UAE (CBUAE) has introduced regulations to make the adoption of IFRS 9 smoother. These include the “Prudential Filter” and credit risk management rules that protect financial stability.

UAE Laws Governing ECL and IFRS 9

The UAE has specific laws to support businesses implementing ECL under IFRS 9:

1. Accounting Provisions and Capital Requirements Regulations:

The regulation introduces the Prudential Filter. The Prudential filter is a temporary measure to help banks and finance companies transition smoothly to the Expected Credit Loss (ECL) model under IFRS 9. It allows businesses to gradually integrate increases in ECL provisions into their regulatory capital over five years.

Without this filter, the sudden recognition of higher credit loss provisions could impact a bank’s regulatory capital, potentially destabilising its financial position. The Prudential Filter ensures financial stability by spreading out the effect over time.

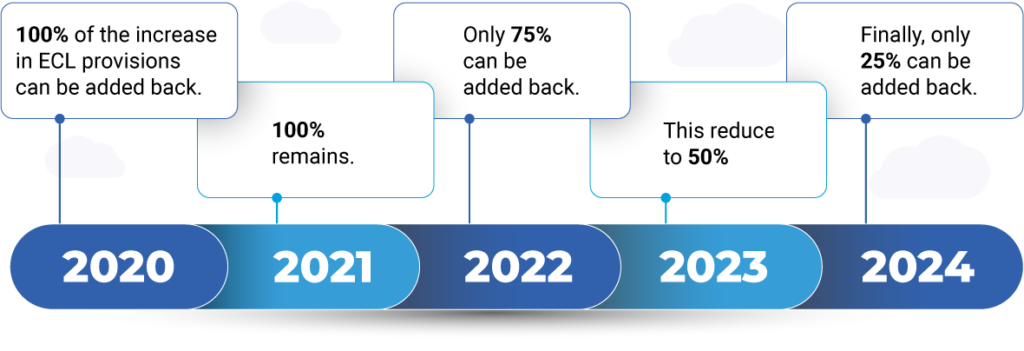

What is Phased Implementation?

Phased implementation refers to the gradual process of applying the impact of ECL provisions to regulatory capital over a defined period. Instead of absorbing the full effect of increased ECL provisions in one go, you can “add back” a percentage of these provisions to your capital, reducing the immediate financial strain.

Let us assume the calculations are implemented for the 5 years between 2020 to 2025.

From 2020 to 2024, You can add a declining percentage of ECL provisions to regulatory capital:

The Prudential Filter ends by 2025, and your business must fully comply with IFRS 9. No ECL provisions can be added back to regulatory capital. Implementing ECL requirements such as The Prudential Filter and phased implementation introduced by the Central Bank of the UAE (CBUAE) give your business in the UAE time to adapt to the forward-looking ECL framework while maintaining regulatory capital strength.

2. Credit Risk Management Regulation:

The regulation ensures businesses, especially banks and finance companies, manage credit risks effectively to prevent unexpected financial losses.

Key Requirements:

- Board Responsibility: The board of directors must oversee and approve credit risk strategies to ensure compliance.

- Management’s Role: Management must implement systems to evaluate credit risks. They also have to ensure that ECL provisions are realistic and based on customer behaviour and market trends.

This regulation helps businesses align their operations with the best practices in risk management.

3. CBUAE Guidance on IFRS 9 Application

The UAE government issued the CBUAE guidance during the COVID-19 pandemic to address economic uncertainties and support businesses in implementing IFRS 9.

Why Was It Introduced?

The pandemic caused significant changes in market conditions, like GDP fluctuations and industry downturns, which affected businesses’ ability to calculate ECL accurately.

Focus Areas:

- Encourages businesses to incorporate forward-looking risks (e.g., GDP changes, inflation) into their ECL calculations.

- Provides practical steps to ensure that ECL reflects real-world economic conditions.

What These Regulations Mean for UAE Businesses

- 1 The Prudential Filter gives businesses time to adapt to higher ECL provisions, protecting their capital during the transition.

- The Credit Risk Management Regulation ensures businesses maintain strong risk management systems to handle credit uncertainties.

- The CBUAE Guidance helps businesses incorporate realistic and forward-looking risks into their ECL calculations, ensuring transparency and stability.

Together, these rules ensure that businesses in the UAE comply with IFRS 9 while safeguarding their financial health.

Practical Steps for Your UAE Business to Implement ECL requirements:

Preparation is crucial, and so is compliance. To save your time and double trouble while implementing

ECL under IFRS 9, we suggest these practical steps:

Collect Data

To calculate ECL effectively, you need to gather key information about your financial assets:

- Understand receivables, payment terms, and customer credit ratings.

Example: If a customer owes AED 500,000, with a Probability of Default (PD) of 3% and Loss Given Default (LGD) of 60%, you’ll need this data to calculate ECL accurately.

Group Customers by Risk

Segment customers into groups with similar risk profiles. This step makes calculations more precise and manageable.

- Base your grouping on payment behaviour, industry, or credit history.

Example: You might separate retail clients (short-term payments) from wholesale clients (long-term credit).

Automate Calculations

Manual ECL calculations can lead to errors. Automating this process saves time and ensures consistency.

- Use ERP systems or accounting software to streamline calculations.

Example: Automated systems can instantly update ECL when payment terms or economic conditions change.

Adjust for Macroeconomic Factors

ECL calculations must reflect the broader economic environment.

- Consider factors like oil price trends, inflation, or global economic shifts.

Example: During an economic downturn, risks may rise, requiring updated ECL models.

Follow Local Rules

Adhering to UAE-specific regulations is crucial.

- Use the Prudential Filter to phase in ECL provisions and reduce the impact on your capital.

- Align your processes with the Central Bank of the UAE’s guidance.

Challenges in ECL Implementation

While implementing ECL requirements, you may face these challenges. You can overcome them with strategic solutions:

Limited Data

Many businesses need more detailed customer credit information, making ECL calculations harder.

Solution: You should partner with credit insurers or external rating agencies to get reliable data.

Forward-Looking Adjustments

Predicting future risks, like economic downturns, can be complex.

Solution: Work with experts such as NNCA who can provide accurate macroeconomic forecasts to adjust your models.

Manual Processes

Relying on manual calculations increases the likelihood of errors.

Solution: You can Automate data collection and processing with advanced tools to save time and improve accuracy.

Avoiding Double Counting Risks

Double counting risk occurs when the same risk factors are included multiple times in Expected Credit Loss (ECL) calculations, leading to inflated provisions. The risk occurs when you use overlapping assumptions, data sources, or methods without proper alignment. Double counting distorts financial statements and impacts regulatory compliance and decision-making.

How Double Counting Risk Happens:

- Duplicate Inclusion of Risk Factors

- Inconsistent Data Sources

- Layering of Models

- Overestimating Forward-Looking Risks

How to Avoid Double Counting Risk

- Standardise Inputs Across Departments

- Use consistent data for key variables like PD, LGD, and macroeconomic factors across all teams.

Example: Ensure credit and accounting teams work with the same GDP growth projections.

2. Reconcile Risk Models

- If you use multiple models, review them holistically to identify and eliminate overlaps.

Example: Combine internal credit scoring with external ratings instead of applying both separately.

3. Implement Clear Governance

- You have to define processes to ensure that risk factors are accounted for once, with clear roles and responsibilities for teams.

Example: Create a centralised team to oversee ECL calculations and data usage.

4. Validate Models Regularly

- Conduct frequent tests to check for redundancies in risk assumptions or overlapping calculations.

Example: Review PD and LGD assumptions to ensure macroeconomic adjustments aren’t double applied.

5. Collaborate Across Functions

- Foster communication between accounting, risk management, and credit teams to align methodologies and assumptions.

Example: Jointly review ECL models before finalising provisions.

Example of Double Counting Risk

A UAE-based trading company supplies goods to various clients, including a large retail chain. The company assesses this client’s credit risk using both internal credit scoring and external credit ratings.

Potential Double Counting Issue:

- Internal Credit Scoring: The company’s internal model evaluates the client’s financial health, considering payment history and current economic conditions.

- External Credit Ratings: The company also refers to external ratings that incorporate similar financial health indicators and economic factors.

If both assessments are used independently in the ECL calculation without proper alignment, there is a risk of double-counting the same credit risk factors.

Impact:

This overlap can lead to overestimating the client’s credit risk, resulting in higher ECL provisions than necessary. Such inflated provisions can reduce reported profits and may misinform management decisions.

Solution:

- Integrate Assessments: Combine insights from both internal and external evaluations to form a unified view of the client’s credit risk.

- Avoid Redundancies: Clearly define which assessment contributes specific information to the ECL model to ensure that overlapping risk factors are not double-counted.

You can prevent double counting by carefully integrating multiple credit risk assessments, leading to more accurate ECL calculations and better financial decision-making.

How NNCA Can Help?

At NNCA, we help UAE businesses such as yours implement ECL requirements under IFRS 9 by:

- Designing practical ECL models.

- Automating data collection and calculations.

- Ensuring compliance with CBUAE regulations such as the Prudential Filter.

Conclusion

ECL under IFRS 9 is essential for modern financial reporting. For UAE businesses, understanding and applying the rules ensures compliance and protects financial stability. With UAE-specific laws like the Prudential Filter and expert support from NNCA, your business can adapt ECL seamlessly and prepare for future risks.

Contact NNCA today for ECL solutions that simplify compliance and strengthen your financial reporting.